When you’re tracking your own finances, you’re only accountable to yourself. When you’re managing money with a partner, your financial choices need to be justifiable to your partner, too. This adds a degree of difficulty to an already complicated task.

Tracking expenses is more than watching your account balance drop every day until replenished by your next paycheck. You need to know where every dollar goes and make sure your spending is in line with each other’s financial priorities. There are different ways of tracking expenses that work for different personality types. You’ll need to pinpoint a method that works for you and your partner.

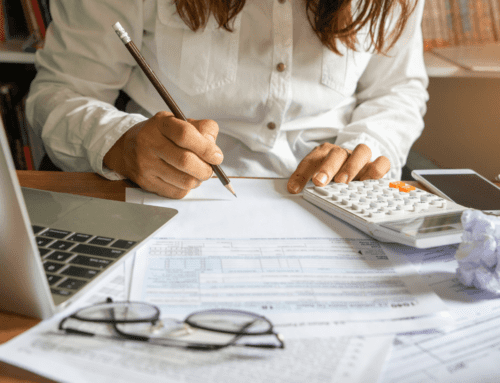

Tracking Apps

Luckily, these days, tracking financial transactions is much easier than writing down every deposit and withdrawal in a checkbook like your parents and grandparents. You can check your balance on a mobile banking app, on a computer, or at an ATM. But there are also specialty apps that can make the process a little more pain-free. Many of these apps are free, with the option to pay for added features or insights. Financial apps typically require more time to set up, so research options first and find one that is a good fit before diving in. Also, some of the most effective apps require access to your bank, credit, and other accounts to accurately track your spending. Be sure to read reviews and make sure the apps are secure and effective before you start entering personal information.

Think through how you prefer to organize your finances when assessing an app. Do you like to organize your spending by category, like groceries or subscriptions, so you know exactly what you can spend in each area? Or do you prefer to focus on what you actually have available to spend as discretionary income after all of your bills are accounted for?

Apps to Consider

Difficult Conversations

If your transactions aren’t lining up with financial priorities, it may be time to have an honest conversation with your partner and make sure you’re on the same page when it comes to finances. The conversation should involve both of you taking responsibility for your finances. It could include discussions about:

- setting financial goals for saving and spending

- deciding who will pay bills and monitor account balances

- determining what amounts to allocate to budget categories

- outlining how to deal with unexpected expenses

Hopefully, once you’ve identified any issues, it’ll be easier to make adjustments that serve you well going forward. You may need to compromise on certain categories so that the budget works for your partner—even if you prefer to spend less or more when managing money solo.

Password Sharing

It’s never a good idea to share your passwords with others—the one exception is knowing the passwords to all your shared accounts, even those your partner manages. Make sure you know how to access joint bank and investment accounts, and any other apps or money management software you use for joint funds.

Best practices for passwords still apply. To that end, it may be a good idea to use an electronic password manager that you can both access on a computer or mobile device, using one universal password instead of tracking many. You could also keep a paper list of passwords somewhere secure, like a home safe. Don’t forget to include passwords for household accounts, like utility accounts, in addition to passwords for bank and investment accounts.

Tracking joint expenses may be complicated, but good communication and planning can take the stress out of the process.

While we hope you find this content useful, it is only intended to serve as a starting point. Your next step is to speak with a qualified, licensed professional who can provide advice tailored to your individual circumstances. Nothing in this article, nor in any associated resources, should be construed as financial or legal advice. Furthermore, while we have made good faith efforts to ensure that the information presented was correct as of the date the content was prepared, we are unable to guarantee that it remains accurate today.

Neither Banzai nor its sponsoring partners make any warranties or representations as to the accuracy, applicability, completeness, or suitability for any particular purpose of the information contained herein. Banzai and its sponsoring partners expressly disclaim any liability arising from the use or misuse of these materials and, by visiting this site, you agree to release Banzai and its sponsoring partners from any such liability. Do not rely upon the information provided in this content when making decisions regarding financial or legal matters without first consulting with a qualified, licensed professional.

![Envelope Budgeting [Cash vs. Digital]](https://b3271481.smushcdn.com/3271481/wp-content/uploads/2024/04/evenvelop-budgeting-1-500x383.png?lossy=2&strip=1&webp=1)